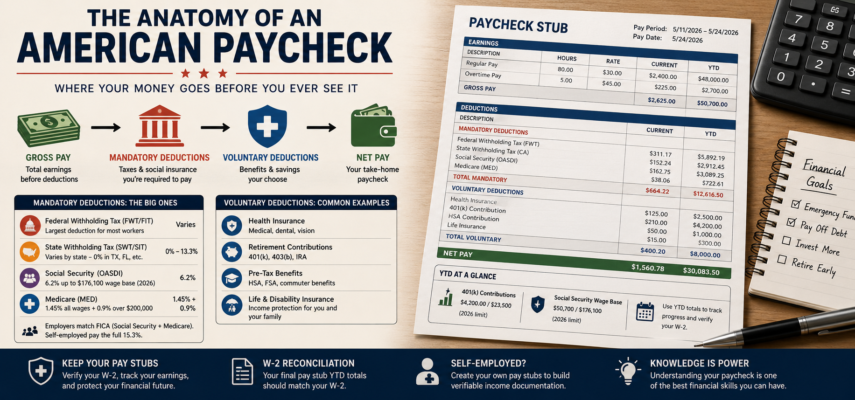

For most American workers, the number on their employment offer letter and the number that lands in their bank account are two very different figures. Between gross pay and net pay sits a complex system of federal taxes, state taxes, social insurance contributions, and voluntary deductions that quietly reshape every paycheck before the worker ever sees it.

Understanding that transformation is one of the most useful forms of financial literacy a person can develop. Yet surveys consistently show that most workers cannot accurately explain the deductions on their own pay stub. Let us break down the anatomy of an American paycheck, line by line, and visualize exactly where the money goes.

From Gross to Net: The Big Picture

Gross pay is the starting point: total earnings before anything is removed. For a salaried employee, it is the annual salary divided by the number of pay periods. For an hourly worker, it is hours worked multiplied by the hourly rate, plus any overtime calculated at 1.5 times the regular rate for hours beyond 40 in a week.

From that gross figure, deductions fall into two broad categories: mandatory withholdings (taxes the employer is legally required to remove and remit) and voluntary deductions (benefits the employee has elected, such as health insurance and retirement contributions). What remains after both categories is net pay, the actual take-home amount.

The proportions vary dramatically depending on income level, state of residence, and benefit elections. A worker in a no-income-tax state like Texas or Florida keeps a meaningfully larger share of gross pay than an equivalent earner in California or New York, purely because of the state tax line.

Decoding the Abbreviations

Open any pay stub and you are confronted with a wall of acronyms: FWT, SWT, OASDI, MED, FICA, YTD. These abbreviations are standardized enough to appear on nearly every American pay stub, yet opaque enough that most workers never learn what they mean.

The most common ones break down as follows:

- FWT / FIT: Federal Withholding Tax, the largest deduction for most workers

- SWT / SIT: State Withholding Tax, which varies enormously by state

- OASDI: Old-Age, Survivors, and Disability Insurance, the formal name for Social Security

- MED: Medicare tax

- YTD: Year-to-Date running totals

For a complete reference, this guide to paycheck stub abbreviations decodes every code a worker is likely to encounter. Understanding them is the difference between blindly trusting a paycheck and being able to verify it.

The Social Insurance Layer: FICA

FICA, the Federal Insurance Contributions Act, bundles two separate payroll taxes that fund America’s largest social programs. Social Security is taxed at 6.2% of wages up to an annual wage base of $176,100 in 2026, while Medicare is taxed at 1.45% on all wages with no cap, plus an additional 0.9% on earnings above $200,000.

Employees pay half of these amounts and employers match the other half, which means the true cost of FICA is double what appears on the pay stub. Self-employed workers feel this acutely, because they pay both halves themselves, a combined 15.3% known as the self-employment tax.

The distinction between the two taxes confuses many workers who see both lines and assume they are being double-taxed. In reality, FICA vs Medicare represents two different programs with different rates, different wage bases, and different rules, all bundled under one umbrella term.

The Numbers That Track You All Year: YTD

Every pay stub carries year-to-date columns that accumulate from January 1st through the current pay period. These figures are easy to overlook, but they function as a real-time financial dashboard.

The year-to-date totals let a worker track progress toward the 401(k) contribution limit of $23,500 in 2026, anticipate the point at which Social Security withholding stops after hitting the wage base, and verify their W-2 at year-end by comparing it against the final pay stub of the year. For anyone managing their finances deliberately, the YTD column is the most useful data on the entire document.

The Year-End Reconciliation: The W-2

At the close of the calendar year, all of this pay stub data consolidates into a single document: the W-2. It is the form workers use to file their tax returns, and its figures should reconcile precisely with the year-to-date totals on the final pay stub of December.

Employers are legally required to issue W-2s by January 31st. Understanding how to fill out a W-2 form (or how to read one) helps workers catch discrepancies before they file, since an error on the W-2 can delay a refund or trigger an IRS notice. The most important boxes are Box 1 (taxable wages), Box 2 (federal tax withheld), and Boxes 3 through 6 (Social Security and Medicare wages and taxes).

What Happens When There is No Pay Stub

The entire framework above assumes a traditional employer-employee relationship. But the American workforce is shifting. Tens of millions of people now earn income through freelancing, gig platforms, and independent contracting, and none of them receive an employer-generated pay stub.

For these workers, income arrives as a patchwork of client payments and platform payouts with no taxes withheld and no documentation tying it together. This creates a measurable disadvantage: self-employed individuals are denied apartments and loans at higher rates than traditional employees with equivalent income, simply because they lack recognizable documentation.

The practical solution is for self-employed workers to generate their own records. By paying themselves a consistent amount from a business account and using a tool to create pay stubs online, independent earners can produce the same standardized income documentation that traditional employees receive automatically, transforming scattered deposits into a clean, verifiable record.

Why Your Pay Stub is Worth Keeping

Pay stubs are not disposable. They are the primary evidence in wage disputes, the documentation lenders request for mortgages, and the records that verify your Social Security earnings history. The general guidance on how long to keep your pay stubs is a minimum of one year, until you have reconciled them against your W-2, with many financial advisors recommending longer retention for mortgage applications and Social Security verification.

The Bigger Picture

A paycheck is more than a number. It is a compressed snapshot of the American tax and social insurance system, applied to a single worker, every two weeks. The gap between gross and net pay tells a story about how the country funds retirement, healthcare, and government, and about the choices each worker makes regarding benefits and savings.

Learning to read that story, line by line and abbreviation by abbreviation, is one of the highest-return investments in financial literacy available. The data is already there on every pay stub. The only question is whether you know how to read it.