Photo courtesy of Pexels

Financial emergencies can happen to almost anyone. A sudden car repair, medical expense, job disruption, or unexpected household bill can quickly put pressure on a carefully planned budget. In these situations, stress often leads people to make rushed financial decisions that solve immediate problems but create bigger challenges later.

While every financial situation is different, certain mistakes tend to appear repeatedly during periods of financial strain. Understanding these common pitfalls can help people make more informed decisions when money becomes tight.

Ignoring the Problem for Too Long

One of the biggest mistakes people make is avoiding the situation altogether. Opening bills can feel overwhelming when money is already stretched thin, but delaying action often makes financial problems harder to manage. Missed payments can lead to:

- Late fees

- Interest charges

- Service interruptions

- Lower credit scores

In many cases, contacting creditors early can open the door to payment plans or temporary hardship arrangements before penalties begin accumulating.

Making Decisions Based on Panic

Are you desperate for fast money to pay your bills? Financial stress can create a sense of urgency that pushes people toward quick decisions. Taking even a short amount of time to evaluate available options can help prevent costly mistakes.

When feeling this desperate, it becomes tempting to focus only on the immediate problem rather than the long-term consequences. This can lead to choices such as:

- Taking on unaffordable debt

- Selling important assets too quickly

- Borrowing without understanding repayment terms

- Draining retirement savings prematurely

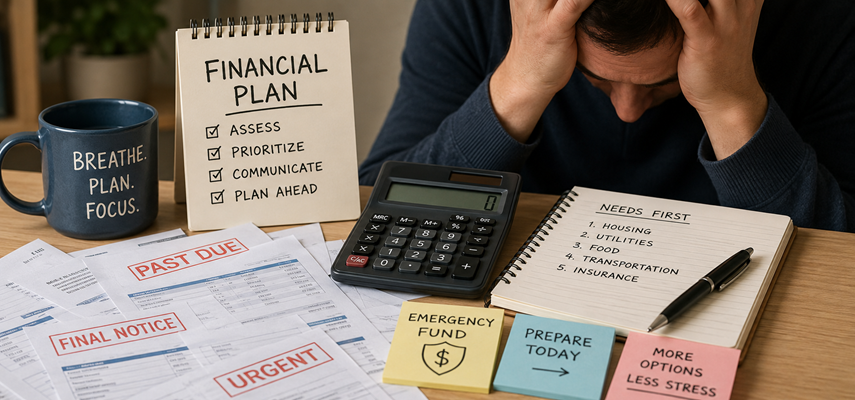

Failing to Prioritize Essential Expenses

During a financial emergency, not every bill carries the same level of urgency. One common mistake is treating all expenses equally when available funds are limited. Non-essential spending often needs to be temporarily reduced until the immediate financial pressure passes. Generally, people should focus first on:

- Housing costs

- Utilities

- Food and groceries

- Transportation needed for work

- Essential insurance payments

Not Communicating With Creditors

Many people assume creditors will automatically reject requests for assistance. In reality, many lenders, utility providers, and service companies offer hardship programs designed to help customers experiencing temporary financial difficulties. The sooner communication happens, the more options may be available. Depending on the situation, companies may offer solutions like:

- Payment extensions

- Temporary payment reductions

- Modified repayment schedules

- Late-fee waivers

Relying Too Heavily on Credit Cards

Credit cards can provide short-term relief, but relying on them heavily during a financial emergency can create long-term debt problems. High-interest balances can grow quickly if repayment becomes difficult. What begins as a temporary solution may turn into months or years of additional financial pressure. Eventually, people find themselves stuck in a vicious cycle where they can never fully pay off their credit card debt.

This does not mean credit cards should never be used during emergencies. However, they are generally most effective when there is a realistic plan for repayment. It’s always important to remember that credit cards aren’t ‘free money’ and eventually need to be repaid.

Forgetting to Build an Emergency Plan Afterward

Once a financial crisis passes, many people return to normal routines without making changes that could help prepare for future emergencies. According to surveys from financial institutions and consumer finance organizations, many households continue to have limited emergency savings despite experiencing financial disruptions.

Building even a small emergency fund over time can help reduce the impact of future unexpected expenses. The goal is not necessarily to save thousands of dollars immediately, but to create a financial cushion that provides more options when challenges arise.

Endnote

Money emergencies can be stressful, but the decisions made during those periods often have long-lasting effects. Ignoring problems, borrowing impulsively, or failing to communicate with creditors can make difficult situations even harder to manage.

While there is rarely a perfect solution during financial hardship, taking a measured approach, prioritizing essential expenses, and exploring available options can help people navigate short-term challenges without creating larger financial problems in the future.